Thai Banks Trade Lower amid Rising Concerns over High Provision to Pressure 2Q Earnings

The banking sector in the Thai stock market edged lower in the morning session on July 7 amid rising concerns over lower 2Q earnings.

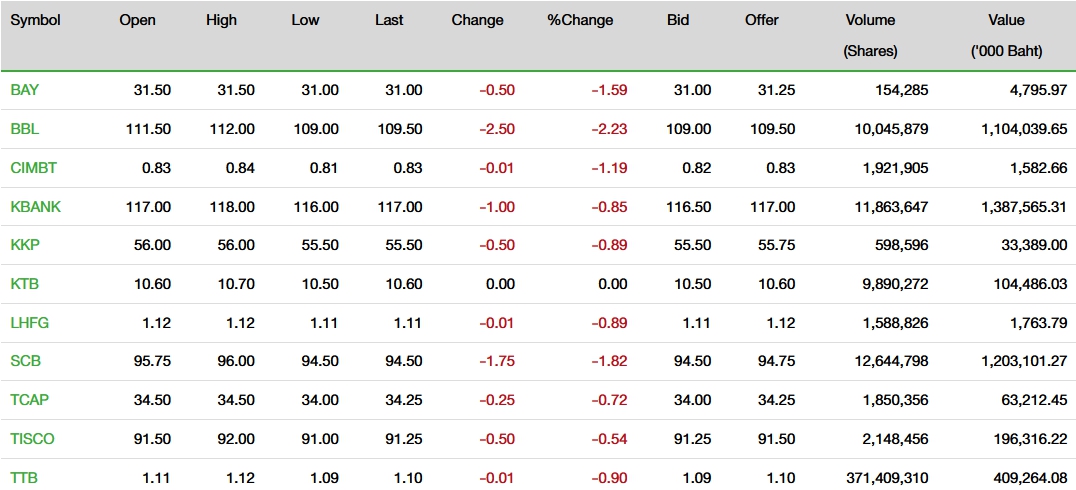

The banking sector all plunged in the morning session on July 7, 2021, in concerns of lower 2Q21 earnings due to higher provisioning expenses and lower loan yield to pressure NIM for big banks.

KGI Securities had a neutral view on the Thai bank, stating that excluding Bank of Ayudhya (BAY), it expected the earnings of most banks to decline around 16% QoQ due to high base trading gain and FVTPL booked in 1Q21 and higher provisioning expense in 2Q21F, while expecting solid YoY growth of 42% due to high base provisioning expense and the sharp fall in fee income in 2Q20.

For 2Q21F, the earnings growth factors in slight pressure on NIM as big banks Krungthai Bank (KTB), Bangkok Bank (BBL), Kasikornbank (KBANK) grew more loans in low-yield money market lending, and realized lower EIR for troubled borrowers. Meanwhile, fee income from the capital market should help partly offset the NII shortfall.

Among big banks, Siam Commercial Bank (SCB) and TMBThanachart Bank (TTB) would see a decline in NIM in 1Q21 due to a lower effective loan rate (EIR) for troubled borrowers mostly in H/P, mortgage loan, and SME. Given the further weakening in economic conditions in 2Q21, providing loan extensions to troubled borrowers will pressure their yields again in 2Q21F.

However, KGI Securities see different reasons for pressure on the yields at KTB and BBL as they have been growing lending in low-yield money market loans which rose 13%/21% QTD for KTB/BBL in May 2021.

Core banking fees in loan related fees and transaction fees are expected to be weak at all banks in 2Q21, but this should be offset by fees from the capital market i.e., AM fees, brokerage fees, IB fees, bancassurance. The banks that have high exposure of >40% to these types of fees (SCB, TTB, BBL, and KBANK) should continue to grow these fees and boost all6in fee income growth to around >10% YoY in 2Q21. With a highly volatile on capital market, we expect trading gains for derivative business for Kiatnakin Phatra Bank (KKP).

In the meantime, KGI Securities expected asset quality to be favoured by regulation as the Bank of Thailand (BoT) continued to relax regulations on loan reclassification for banks providing debt assistance during the third wave of COVID619. This should allow the banks to gradually manage credit costs at a moderate level.

KGI Securities expected higher credit costs of +40bps QoQ for KBANK, +20bps for KKP, +10bps for TTB and KTB, while SCB and BBL should remain stable at a high level for the third straight quarter.

In addition, KGI Securities stated that KBANK remained its top pick in the sector. Though there would be pressure on its NIM, growth should be driven by capital market fees and squeezed operating expenses, and weighting potential revenue growth and risk of provisioning expenses.