PTTEP – A Chance to “Buy the Dips” or “Sell before Hitting Rock Bottom”

PTTEP was the bidding winner for the operator of Bongkot-Erawan natural gas fields, but the stock markets do not share the same enthusiasm as the company, plunging the share over and over, while brokers still have positive views on PTTEP.

On December 13, 2018, the Ministry of Energy made an announcement regarding the acquisition of PTTEP in Bongkot-Erawan natural gas fields. Later, PTTEP’s shares plunged continuously, raised questions on whether the acquisition of both natural gas fields was actually good for PTTEP or not.

The share had plunged 10% since December 13, from the worry of the “winning by dumping” may not worth much for PTTEP’s investment. Especially, the constant price at ฿116/MBTU on both fields has a huge difference compared to the current price of ฿214.26/MBTU for Bongkot field and ฿165/MBTU for Erawan field.

Regarding the matter of lower constant price, Mr. Phongsthorn Thavisin had asserted on “Kaohoon Live” last Friday that the price at ฿116/MBTU was “worthwhile”, even though the return per unit might decrease.

The decreasing in price is relevant with the new operation contract, indicating the new operator to be able to use the existing systems and drilling platforms without any further investment in the first phase, conforming with the previous contract which states that the former operator must hand over drilling platforms to the government at the end of concession, so that the government can lend it to the new operator at a reasonable price.

Moreover, the concession in both fields is considered an increase in production capacity that PTTEP has never done before, creating a “synergy” to increase sales volume and compensate the loss from a lower constant price. The production from both fields will also increase PTTEP’s gas reserves for sales, as well as the decrease in production cost according to Economics of Scale.

“The company will benefit from 20-25% lower administration cost and increasing of negotiation power in terms of procurement or shipment on par with more and constant projects. These acquisitions also reduce the production cost from drilling, supplying and services,” said Mr. Phongsthorn.

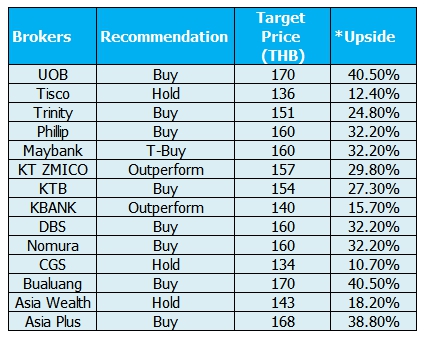

The majority of analysts also gave positive views on this matter. Out of 14 brokers, 11 brokers recommended “Buy” while the other three recommended “Hold”

As for the international securities like Phatra also upgraded its target price from ฿156/share to ฿173.70/share, while Morgan Stanley ranked PTTEP “attractive” with a target price at ฿163.00/share.