DTAC Reports a Robust 2Q Profit at ฿1.8Bn from Lower SG&A, Offering a ฿0.87 Dividend

DTAC Reports a Robust 2Q Profit at ฿1.8Bn from Lower SG&A, Offering a ฿0.87 Dividend.

Total Access Communication Public Company Limited (DTAC) has reported its consolidated financial statement of 2Q20 through the Stock Exchange of Thailand as follows;

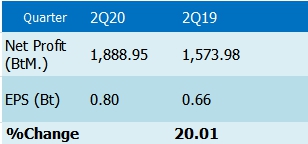

In the second quarter of 2020, DTAC recorded a net profit of THB 1,889 million, increased 20%, when compared to a net profit of 1,573 million baht in 2Q19.

Total revenues in Q220 amounted to THB 19,160 million, reducing 4.6% QoQ and 4.3% YoY from a drop in service revenue as well as handsets and starter kits sales. The reduction was slightly offset by higher other operating income from TOT 2300 MHz network rental. Service revenues excluding IC decreased 4.5% QoQ and 3.6% YoY down to THB 14,630 million.

SG&A expenses in Q220 amounted to 3,137 million, decreasing 14.2% QoQ and 12.2% YoY. The reduction QoQ is largely accounted by lower selling and marking, general administrative expense, and provision for bad debt.

At the end of Q220, total active subscriber base stood at 18.8 million, a decline of 835k from the end of Q120 due to full impact from COVID-19 affecting new customer acquisition. The majority of subscriber base

decline was prepaid at 757k while postpaid showed a decline at 78k. Approximately 32.3% of total subscriber base were postpaid subscribers.

Average Revenue per User excluding IC (ARPU) for Q220 was THB 253 per month, which was relatively flat QoQ and a slight growth of 1.5% YoY. At the end of Q220, postpaid subscriber base accounted for approximately 32.3% of total subscriber base. Postpaid ARPU for Q220 was THB 525 per month, reducing 0.7% QoQ and 1.4% YoY, while prepaid ARPU was THB 125 per month, showing a drop of 4.1% QoQ and 8.5% YoY, driven by overall optimized customer spending which affected prepaid more than postpaid.

Traffics on TOT’s 4G-2300MHz network continued to increase, driven mainly by people working from home during COVID-19 crisis. No. of 4G-2300MHz installed base stations under the partnership with TOT reached approximately 18,000 at end of Q220. The number of 4G users was 11.4 million, representing approximately 61% of total subscriber base. The number of 4G compatible device increased to 81% of total subs base. Smartphone penetration is now at 87%.

Service revenues excluding IC in Q220 dropped 4.5% QoQ and 3.6% YoY. Core service revenues (defined by bundle of voice and data service revenues) in Q220 reduced 3.3% QoQ and 1.1% YoY from full COVID-19. Blended ARPU stayed relatively flat at 0.5% QoQ and 0.7% YoY in Q220.

In Q220, EBITDA (before other items) improved 5.1% QoQ and 4.2% YoY despite revenue decline, overall reflecting our ability to continue managing cost optimization during the difficult time.

EBITDA margin for Q220 was 42.1%. However, excluding revenues from CAT lease agreements and TOT network rental, EBITDA margin stood at 48.8%.

In addition, DTAC announced a dividend payment from the operations in the first half of 2020 at a value of THB 0.87 per share. The ex-dividend date will be on 24 July, 2020, and the payment date will be on August 14, 2020.